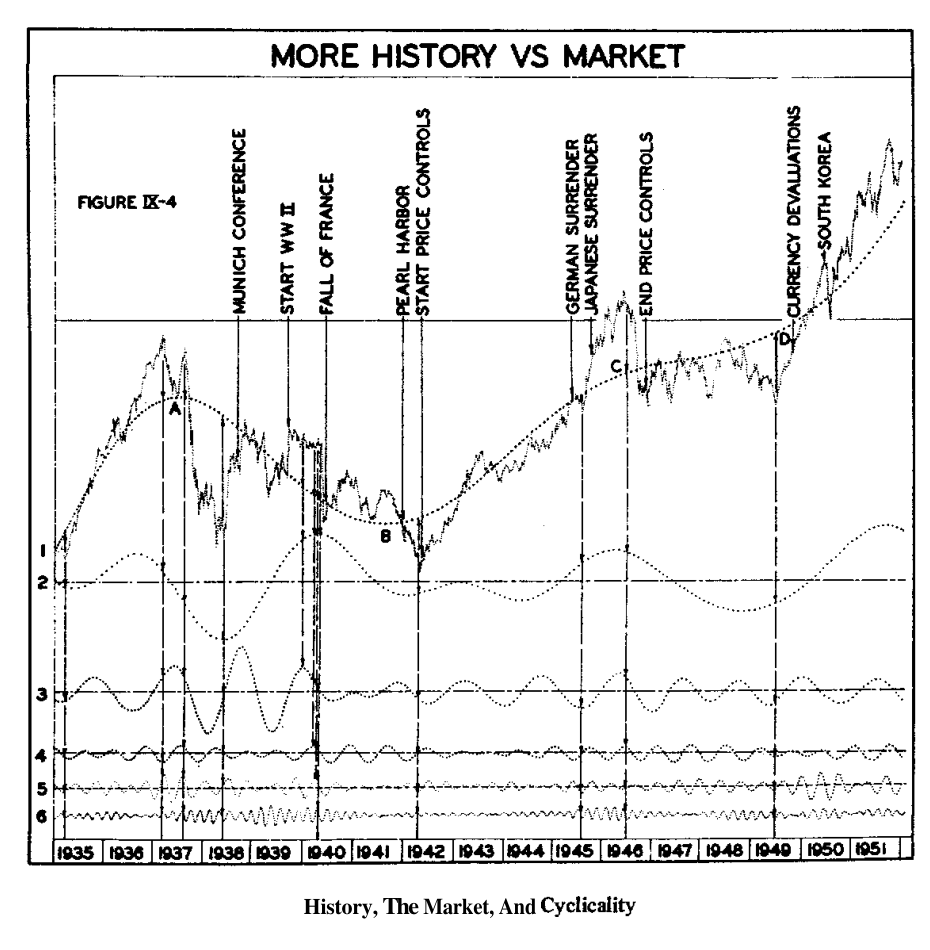

Who this entry is for — "One of the most informative charts in this book", worthy of "intense study": 17 years of Dow decomposed into six regular waves whose sum reproduces price within 1%. It is the empirical proof that cyclicality is not rhetoric — and that not even World War II shows, from price alone.

Source: J. M. Hurst, The Profit Magic of Stock Transaction Timing, Prentice-Hall, 1970 — Chapter 9, §§ Now Compare Cyclicality vs. History! → Here is How Long-Range Cyclicality Affects the Market (pp. 151–157, Fig. IX-4).

Prerequisites

Why prices change, the nominal cycles and — for the sense of the proof — the X motivation.

The three-million-computation chart

In plain words — Weekly Dow closes from 1935 to 1951, the war events overlaid, and six dotted curves: the periodicities identified in the period, extracted with the same techniques used on Warner (Fig. II-11). Question: without peeking at the dates, could you tell when the war was on?

The six components, measured

| # | Measured average duration | Samples | In the nominal model |

|---|---|---|---|

| 6 | 9.6 weeks | 92 in 884 wk | the 6.5-week (shrinking to 6–7 in recent years) |

| 5 | 19.85 weeks | 44½ | the ≈20-week (nominal 26) |

| 4 | 34.6 weeks | 25½ | the ≈9-month |

| 3 | 67.98 weeks (15.7 months) | 13 in 204 months | the 18-month |

| 2 | samples of 38 · 43 · 28 · 54 · 58 months | 5 | the 4.5-year (54 months) |

| 1 | the sum of everything longer than 54 months | — | the 9-year: highs at A and C, lows at B and D |

On component 2 the book points out the effect seen before: the shortest sample (28 months) falls in 1942–44, when the oscillation's magnitude almost went to zero — short durations with low magnitudes, the magnitude-duration fluctuation of the variation principle, seen in the data.

Editor's note — Here the book's arithmetic all checks out: 884 ÷ 92 = 9.61 · 884 ÷ 44.5 = 19.87 · 884 ÷ 25.5 = 34.67 · 204 months ÷ 13 = 15.69 months = 68.0 weeks. The declared averages (9.6 · 19.85 · 34.6 · 67.98) are exact.

The key result: ±1%

"It is perfectly evident that none of the smooth curves one through six are random in nature, yet the sum of these six non-random curves adds up to the curve representing the DJ closing prices within ±1%! If non-random motion makes up all except ±1% of the total price motion, what then is left to be random?"

And the events? Taken one at a time: for 1935–37 no events of major significance could be found — yet the market "roared mightily" and subsided with a thump in 1937–38, price motion "far more extensive than any that took place during all of WW II". The start of the war in 1939 shows no effects: for nearly a year the market drifted sideways. Pearl Harbor (1941) coincides with a plunge — but the market had been going down for months, at the same rate. The German and Japanese surrenders: no impact at all on a rise three years in the making, which neither accelerated nor decelerated.

The fall of France, under the microscope

In plain words — One candidate remains: the fierce, rapid plunge near the fall of France (1940). "The market was discounting the event"? Hurst draws three vertical lines before the event and reads the state of the six components: the plunge was written in the cycles.

| Component | Line 1 | Line 2 | Line 3 |

|---|---|---|---|

| 1 (long) | moving rapidly downward | still down | still down |

| 2 (4.5-year) | over its top → nothing | sideways | sideways |

| 3 (18-month) | hard down | still down | still down |

| 4 (9-month) | over its top → nothing | just starting down | hard down |

| 5 (20-week) | hard up | over the top → nothing | hard down |

| 6 (9.6-week) | hard up | still hard up | just over the top → hard down |

| The market | sideways (a tiny uptick, thanks to 6) | just starting down — gently | "the bottom dropped out" |

"Each of these components had existed and had been oscillating regularly up and down for years before the events leading to the fall of France even had their embryonic beginnings! Was it then anticipation of the fall of France that caused the market to drop?"

Eight turns in 17 years, same grid

The proof in the positive: eight major turning points of the period, read with the same component "scorecard" — the prototype of the state table Chapters 4 and 8 use operationally.

| Case | Turn | Components | Outcome |

|---|---|---|---|

| I | The major rise of early 1935 | all six bottoming or heading up | "No wonder the market went up!" |

| II | The minor drop of early 1937 | mixed; 4–5–6 due to bottom | Fell a little, bounced right back |

| III | The big drop of 1937–38 | nothing up, everything down or topping | "The bottom really dropped out" |

| IV | The up market of 1938 | 3 up vs 3 down — but 2 and 3 larger and longer | Up, less furious than Case I |

| V | The rise of 1942 | 4 up, 2 down (3 soon bottomed) | Up, and it continued |

| VI | The spurt of 1945 | nearly everything up; 2 near a top | Huge but short-lived |

| VII | The hard down market of 1946 | preponderance down; 3 and 4 short | Precipitous but brief |

| VIII | The big up market of 1949 | nearly identical to Case I | Longest, steepest rise since 1935 |

And three reminders alongside the results: they apply strictly to the DJ 30, but the Appendix shows many if not all individual issues behave similarly; the periodicities persist in time, completely independent of all the things we normally think make prices change; and sufficient periodicity spells semi-predictability — that is, transaction-timing aid.

Summary card

| Element | Value |

|---|---|

| Data | DJ 30 weekly closes, 1935–1951 (884 weeks) |

| Extraction | 6 components, >3 million computations, same techniques as Warner (Fig. II-11) |

| Accuracy | sum of the six = price within ±1% |

| Measured durations | 9.6 · 19.85 · 34.6 · 67.98 weeks · 38–58 months · >54 months |

| Fall of France | explained by the cyclic scorecard, before the event |

| Turns 1935–1951 | 8 of 8 consistent with component states |

| The formalism | Ch. 11 — spectral analysis |

Links

- Why prices change — Ch. 9's framework

- Historical events and cyclicity — the same test on 1949–1968

- Cyclic X motivation — what this chart proves

- The nominal cycles — the table the measured durations confirm

- Spectral analysis — the formalism (Ch. 11)

- Hurst tradition — chapter index