Who this entry is for — After the field trial (Ch. 8) the book changes register: no longer "how", but why it works. This chapter is for the bad days — when emotions press and the market refuses to do what you expect.

Source: J. M. Hurst, The Profit Magic of Stock Transaction Timing, Prentice-Hall, 1970 — Chapter 9, Why Stock Prices Change (pp. 141–157).

Prerequisites

The price-motion model (Ch. 2) and, for context, the Ch. 8 shakedown.

The confidence chapter

In plain words — Understanding causes is unnecessary when everything runs smoothly. It matters when things go wrong: that is when, without a base of credibility, you run straight back to old habits.

Chapters 1–8 delivered the model, the techniques and the operational proof. Chapter 9 fills the remaining gap: "to provide you with increased confidence in and understanding of why the techniques work. Such understanding is not needed when all goes smoothly, but can stand you in good stead if your emotions get out of hand or things don't occur quite as expected."

The first concept to revise is risk. In traditional investing, oscillations are evils to be survived; the only defences are good stocks, faith and patience, and short-term trading is inordinate risk. But if the oscillations "have a personality of their own", with characteristics permitting a certain degree of prediction, the risk of short-interval transactions collapses — and many deeply ingrained traditions go from being prudence to being, themselves, untenable risk.

The anatomy of a decision

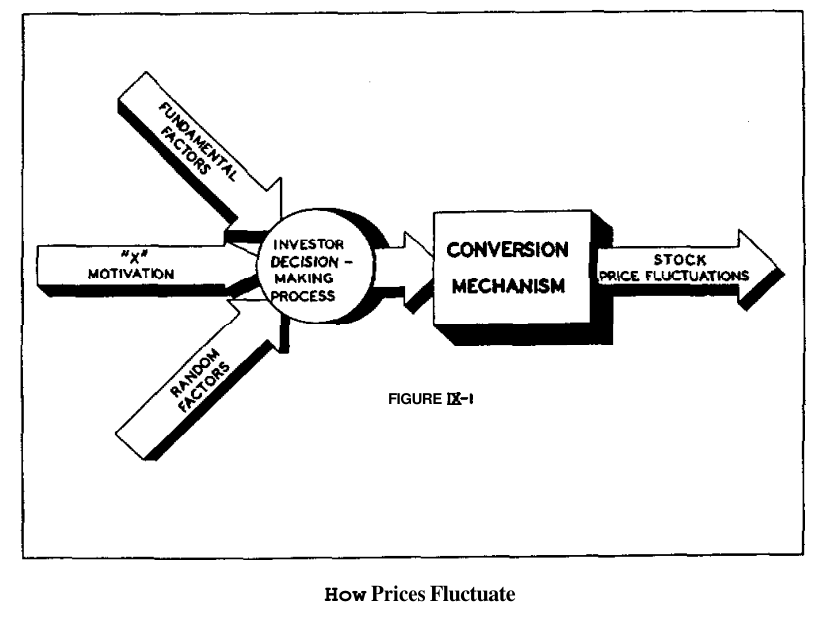

In plain words — Price does not move by itself: every change starts from a decision to buy or sell. Hurst puts everything else (orders, brokers, the exchange) in a box and ignores it: it is machinery, not cause.

Fig. IX-1 is a block diagram. Into the "conversion mechanism" box goes everything between the investor's decision and the consummated trade; price change is the box's output. The processes inside are the direct but not the elemental cause of fluctuations: it is the decision to act that starts the whole process. And the possible contributors to that decision fall under three headings:

- Fundamental factors — people demonstrably buy and sell on research and knowledge of these quantities.

- Random factors — buying merely to place excess funds, selling to raise cash: activity uncorrelated with price level, generating "noise" (≈2% of motion, measured in Ch. 2).

- "X" motivation — everything else, known or unknown. This is where cyclicality lives: the full deduction is in Cyclic X motivation.

The two jobs of fundamentals

In plain words — Fundamentals do two things: push the market's underlying trend and differentiate one stock from another. What they do not — cannot — do is produce regular, synchronized oscillations across different issues.

The chapter distinguishes three classes of fundamental factors: company-specific (new products, management), the company's specialized environment (tight money for a savings-and-loan) and the broad environment (a monetary crisis, armed conflict). None of the three can explain synchronized cyclicality: factors that closely affect one issue but not another cannot be responsible for both oscillating in time-coordination.

Their real weight lies elsewhere. On the single stock, fundamental shocks are large and undeniable — trading suspensions that reopen at half price, tender offers that send a stock flying: "the stock price changed not because of the fundamental factor itself, but because of the effect of that factor on the thinking and decision processes of investors". And since randomness is small and cyclicality synchronized, all other observed differences between individual stock motions must be attributed to fundamentals — or at least to what investors think their effects should be.

On the aggregate market, the fundamental candidate is one: gross national product, strikingly correlated with the Dow's centre line — the part of motion cyclicality does not cover. Details (and caveats) in Historical events and cyclicity.

The chapter's map

| Question | The chapter's answer | Entry |

|---|---|---|

| Where does cyclicality come from? | By exclusion: from "X motivation", the sum of all that is neither fundamentals nor chance | Cyclic X motivation |

| Does news move the market? | No: wars, crises and devaluations leave no imprint on the Dow; the trend correlates with GNP | Historical events and cyclicity |

| And the proof? | The 1935–1951 Dow decomposed into six regular components: the sum returns within ±1% | The DJIA's six components |

Summary card

Card — The chapter's conclusions (p. 157)

- The traditional risk-versus-interval concept is outdated by the model's existence.

- The determining element of price is the human decision process — complex, little understood, with emotions and unrelated influences weighing heavily.

- The cause of cyclicality is unknown; the nature of the effect is certain. And it is probably unrelated to rational decision factors.

- The non-relationship between cyclicality and historical events is clear-cut; specific fundamental events, however, differentiate individual issues and must always be considered.

- True panics (wars, devaluations) are buying opportunities if the cyclic picture is ripe.

- All fluctuations about the market's smooth long-term trend are manifestations of cyclicality.

Warning — If something influences the decisions of masses of investors more or less simultaneously, it influences yours too: "you must guard yourself carefully against the same influences". The direct bridge to Ch. 10's psychological barriers.

Links

- Cyclic X motivation · Historical events and cyclicity · The DJIA's six components

- The price-motion model — the statements grounded here

- Trading by logic — the operational validation (Ch. 8)

- Hurst tradition — chapter index