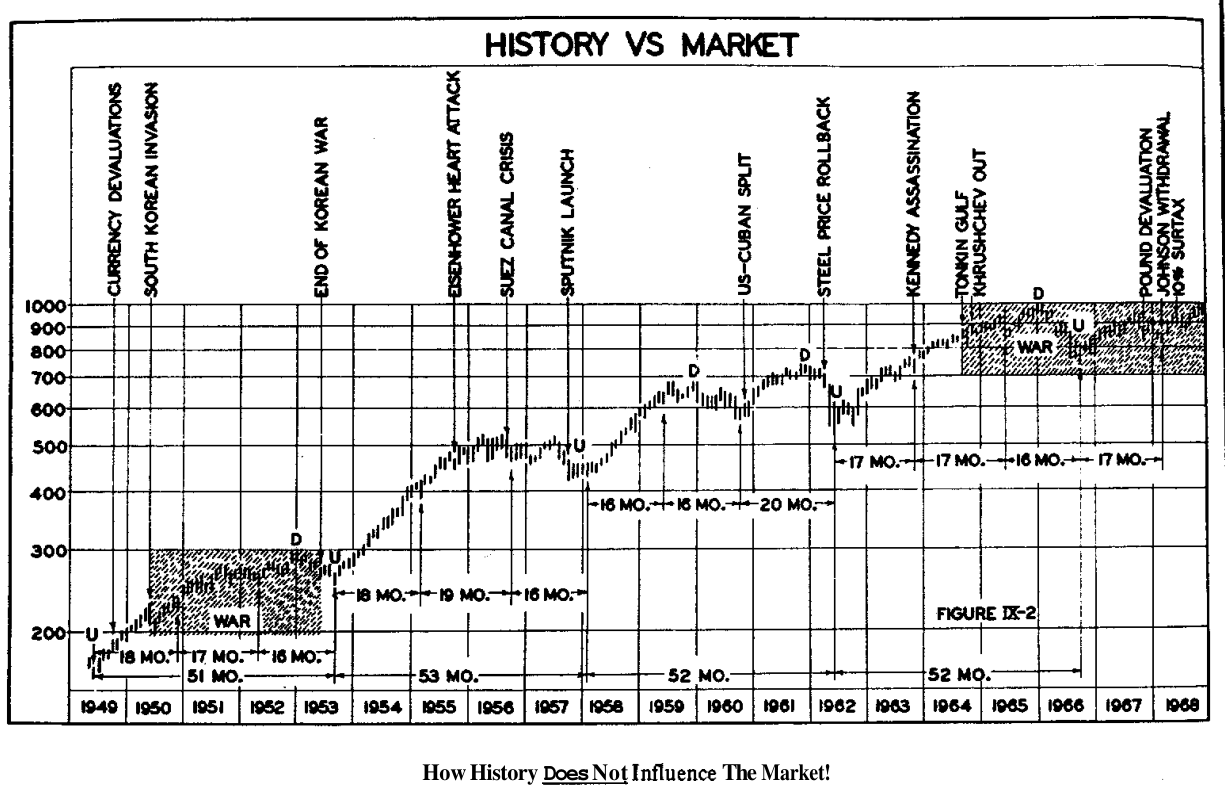

Who this entry is for — Every day the commentaries attribute the market to the news. Hurst runs the counter-test on twenty years of Dow: without the date labels, you could not even find the wars on the chart. If you believe the headlines, that belief distorts your cyclic decisions.

Source: J. M. Hurst, The Profit Magic of Stock Transaction Timing, Prentice-Hall, 1970 — Chapter 9, §§ The Influence of Broad Environmental Factors → How the GNP Affects the Market (pp. 147–151, Figs. IX-2, IX-3).

Prerequisites

Why prices change and the nominal cycles used as the yardstick.

The test

In plain words — The experiment is simple: take the 1949–1968 Dow, overlay the dates of the major events, and ask — with the labels removed, could you tell from price alone when there was a war?

The statement comes from Ch. 2: "national and world historical events contribute in an utterly negligible way to the performance of the market as a whole". That this is an alien concept "is amply illustrated by every financial column and commentary you read and hear", where the market is weak or strong depending on peace talks or ten dozen such factors. But the check is at hand: plenty of recorded price history, and the Almanac supplies the dates.

The wars

During the Korean War a 52-month cycle topped out and ended — exactly as cycles of that family have been behaving since 1897 — complete with its three nested (nominally) 18-month cycles. With Vietnam, a 52-month cycle was about halfway along: it continued and terminated as expected in 52 months' time, "whereupon another promptly started". The book's question: if the news flashed tomorrow that the U.S. was in another war, wouldn't you worry about your stocks? But should you?

The devaluations

In the panic of the 1949 devaluations, an 18-month and a 52-month cycle were both four months along: each continued to completion "in blissful ignorance of the currency troubles". And the pound in November 1967? The market fell, yes — but it was already falling before the devaluation, and that drop was predictable "as much as one and a half years in advance": the terminating phase of a nominally 18-month cycle "that has been going up and down with the regularity of clockwork for nearly a century". The fundamentalist will say the market was "discounting in advance"; the model says it was simply the cycle.

The national crises

| Event | What the chart shows |

|---|---|

| Eisenhower's heart attack (Sep 1955) | The drop coincides with the end of the first of three 18–20 week cycles, in the second of the three 18-month cycles of the 52-month cycle begun in late 1953 |

| US–Cuba split (late 1960) | It was time for an 18-month (here 20-month) cycle to start: it started. The market "disdained even to show the courtesy of a mild reaction" |

| Kennedy's assassination (Nov 1963) | 15 minutes of panic selling, the exchange shut down — yet, in retrospect, the slight drop signalled the expected end of the first 18-month (here 17) cycle of the 52 begun in 1962; then the market "barreled uninterruptedly upward" until the 1965 pullback |

| Suez, Sputnik, Tonkin Gulf, Khrushchev's demise | No identifiable relationship with market activity |

Editor's note — In the book's scan, the Eisenhower episode's cycle reads as begun "late 1963": an evident misprint for 1953 — the heart attack is from September 1955, and the original plate IX-2 prints precisely the "53 MO." span starting in 1953. The paragraph's conclusion, verbatim: "major world and national historical events have negligible impact on stock prices!"

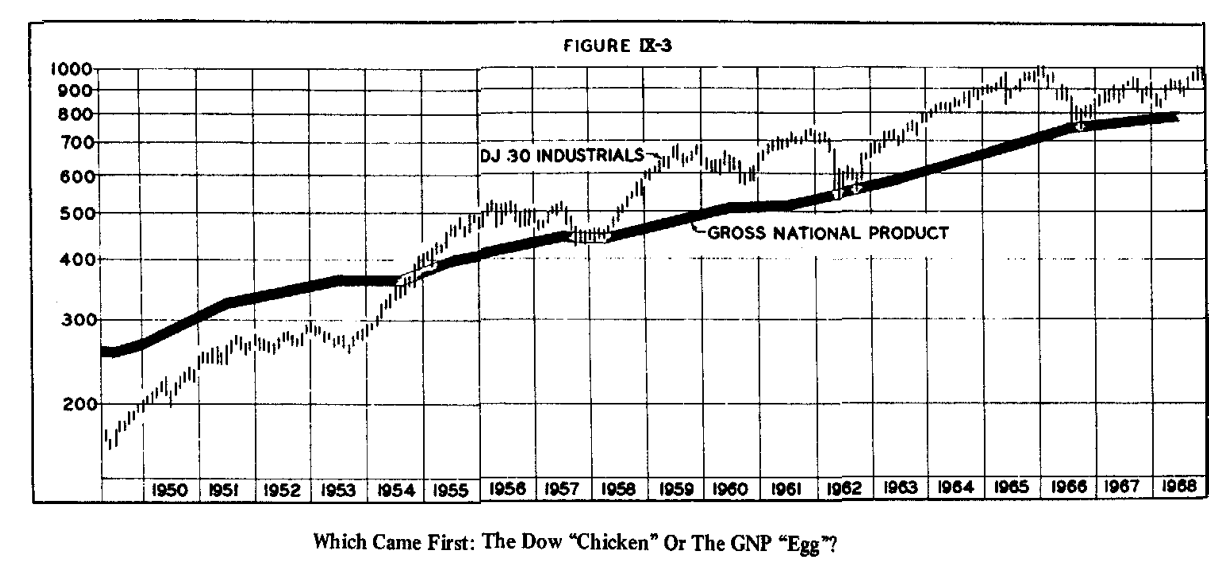

Then what pushes the Dow from 160 to 1000? GNP

In plain words — Cyclicality explains the swings inside the envelope; it does not explain the centre line climbing from ≈160 in 1949 to over 1000 in 1966. The candidate is gross national product — with all due caution.

Overlaying U.S. GNP in billions on the 1949–1968 Dow, the scales match almost perfectly and the correlation is "striking" — there is even a hint of the 52-month cycle's ups and downs in the GNP. The caveats are spelled out: the observed correlation does not necessarily imply cause and effect; both may react to the same causes, or it may be coincidence. But here is a "fundamental" factor that undeniably correlates with market action and seems to account for precisely the part of price motion cyclicality does not: "it certainly stretches the imagination less to impute a relationship here than in the case of historical events".

The operational implication

Card — How to use this lesson

- War or crisis headline: do not flip sides on a news item — check the cyclic state (the three clocks).

- True panic (war, devaluation): it "represents a buying opportunity if the cyclic picture is also ripe" (Ch. 9's conclusions).

- On the single stock, fundamental shocks remain critical: this entry is about the aggregate market.

Links

- Why prices change — Ch. 9's framework

- The DJIA's six components — the same test, under the microscope (1935–1951)

- Cyclic X motivation — where cyclicality comes from

- Cyclic market state — the practice this entry justifies

- Hurst tradition — chapter index