Who this entry is for — The engine of the cyclic 23%: five rules Hurst uses throughout the book to read charts, envelopes and patterns without arbitrariness. They are elements VI–X of the price-motion model.

Source: J. M. Hurst, The Profit Magic of Stock Transaction Timing, Prentice-Hall, 1970 — Chapter 2, Timing Is the Key (pp. 31–34).

Prerequisites

Price motion model — the context of elements I–V. Here we cover the principles governing the cyclic part of the motion.

Before the principles, a definition. When a quantity starts at a low, rises smoothly to a high and descends in the same length of time back to its starting point, it has completed one cycle; if it repeats the action in the same time, we call it cyclic and periodic. The time to complete one cycle is its duration; the entire cyclic activity is a component (p. 32).

1. The summation principle

In plain words — The price you see is the sum of many cyclic waves (about 12) plus the underlying trend. Each wave has its own magnitude, duration and position in time.

Cyclicality in price motion consists of the sum of several non-ideal periodic-cyclic components. Each component differs from the others in three quantities only:

- magnitude — the size of the motion, measured peak to trough;

- duration — the time required to complete one cycle;

- phase — its position in time relative to the others.

At every instant the ordinates of all components, plus the trend, are added: the result is the observed price. It is the move you will repeat most often in cyclic analysis, and it is worth doing by hand at least once:

Example — Raise the short wave's magnitude in the lab: the "gallops" appear — the small zig-zags inside the trend — exactly those of Fig. 1-2 of Alloys Unlimited in Chapter 1.

2. The commonality principle

In plain words — Cycles are no whim of a single stock: similar durations, and highs/lows often synchronized across stocks and indexes.

Summed cyclicality is a factor common to all stocks, expressed in four statements (p. 32):

- cyclicality exists in the price motion of all stocks;

- the components have similar durations from issue to issue;

- cyclic highs and lows are time-synchronized;

- the relative magnitudes of the components are similar in all issues.

The book's most spectacular demonstration is the comparison of Standard Packaging with the DJIA (Fig. II-16): rescaled to the same total variation, the two charts turn together on virtually every duration — "where goeth the Dow, there goeth Standard Packaging". Over the same period, the long cycle measures 70.0 weeks on the stock and 71.0 on the index.

3. The variation principle

In plain words — Cycles are not Swiss watches: magnitude and duration fluctuate slowly, and they do it together. And every stock strays a little from the choir.

Differences between issues come first from the fundamental 75%; the secondary source is deviation from commonality. The heart of the principle is magnitude-duration fluctuation, with the verbatim rule (p. 33): as magnitude increases, duration also increases; as magnitude decreases, duration decreases. Three deviations add to it:

- relative magnitudes and durations differ slightly from issue to issue;

- time synchronization is imperfect (a low may come a few sessions early or late);

- dominance: at a given time some components dominate one issue while others dominate another. In the DJIA 1965–69, for instance, the 9- and 12-month cycles turn out "observationally insignificant" — present, but too small to count.

There is good news inside the principle: extracting the 18-month cycle from the DJIA 1935–1951 by numerical analysis (Fig. II-10), the fluctuation turns out slow and smooth — much slower than the oscillations that make it up. Near-past measurements hold, with prudence, for the near future.

4. The nominality principle

In plain words — Hurst uses a table of reference durations (6.5 weeks, 13, 26, 9 months…). Real cycles oscillate around those values; they do not match them to the decimal.

The effect of variation is to force the use of nominal durations in quantifying the model: common reference values, from which every issue and every era deviate within a range. The complete table — from 18 years down to 1.625 weeks — is in Hurst nominal cycles.

The book's example: on the DJIA 1965–69 the nominal 26-week component shows up as a measured 21.4 ± 3.5 weeks.

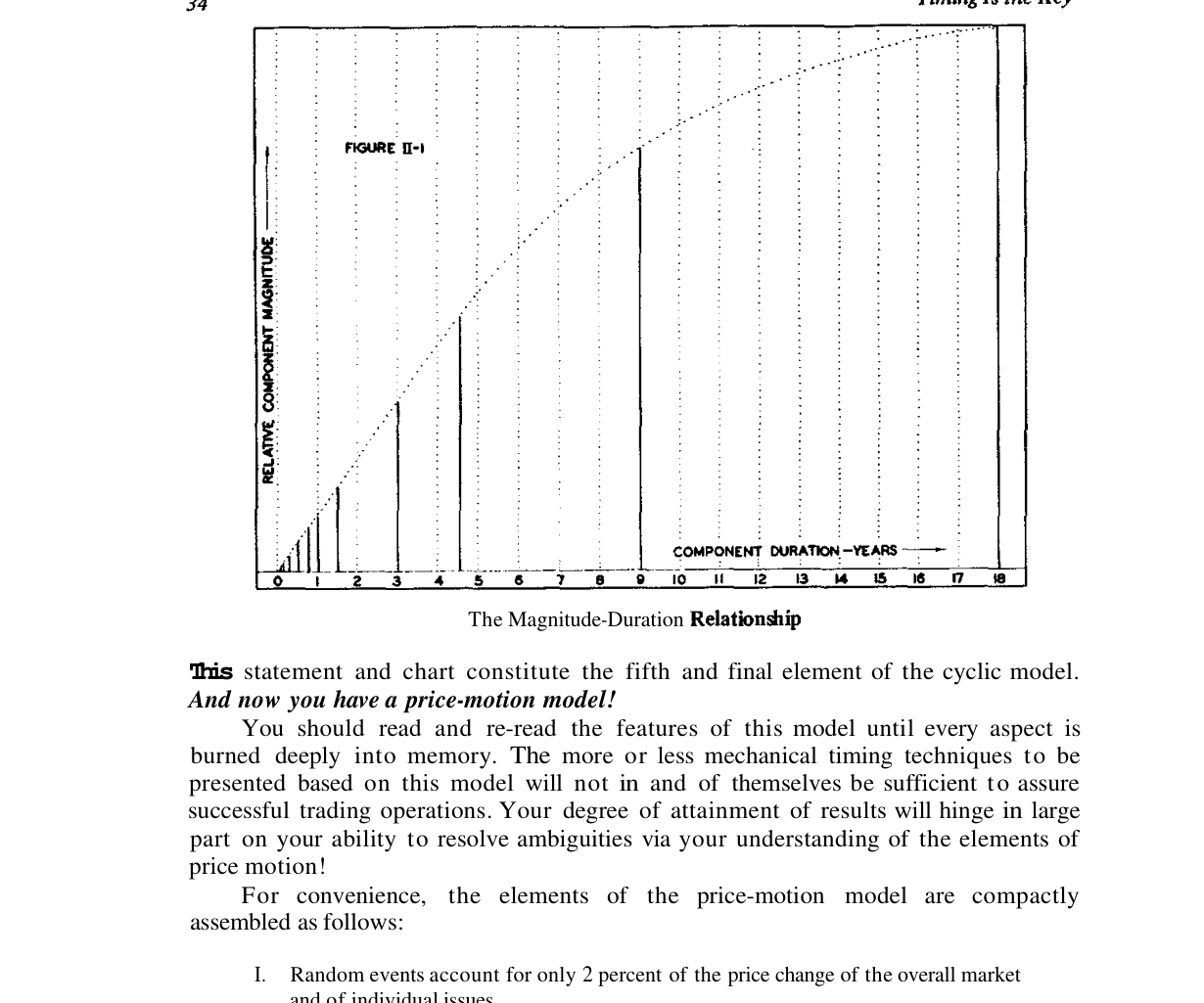

5. The proportionality principle

In plain words — Longer cycle = wider swing. When a 13-week cycle turns, the effect is modest; when the 18-month one turns, you can see it from afar.

The greater the duration of a cyclic component, the larger its magnitude (p. 33). The nominal relationship between the two quantities is the book's Figure II-1:

Why memorize them

Warning — Hurst is explicit: the more or less mechanical techniques of the later chapters are not sufficient on their own. Results hinge on your ability to resolve ambiguities — dominance, fluctuating durations, imperfect synchronization — using these principles as a compass.

Summary card

| Principle | The question it answers |

|---|---|

| Summation | What is cyclic motion made of? Waves that add up |

| Commonality | Is it just this stock? No: all of them, almost in sync |

| Variation | Why do measurements never come out exact? Magnitude and duration fluctuate together |

| Nominality | What ruler do I measure with? The nominal duration table |

| Proportionality | How much will this cycle weigh? The longer, the larger |

Links

- Price motion model — elements I–V

- Hurst nominal cycles — Table II-1

- Curvilinear envelope — how durations are measured on the chart

- Nesting envelope — nested cycles

- Hurst tradition — chapter index