Who this entry is for — One envelope isolates one cycle. To extract the higher cycle and the sub-cycle from the same chart, Hurst nests envelopes inside one another: that is nesting, and with two moves the cycle ladder becomes visible.

Source: J. M. Hurst, The Profit Magic of Stock Transaction Timing, Prentice-Hall, 1970 — Chapter 2 (pp. 38–41, Figs. II-4/II-5/II-6).

Prerequisites

Curvilinear envelope — the first band. Here the second one is built.

Nesting up — the higher cycle

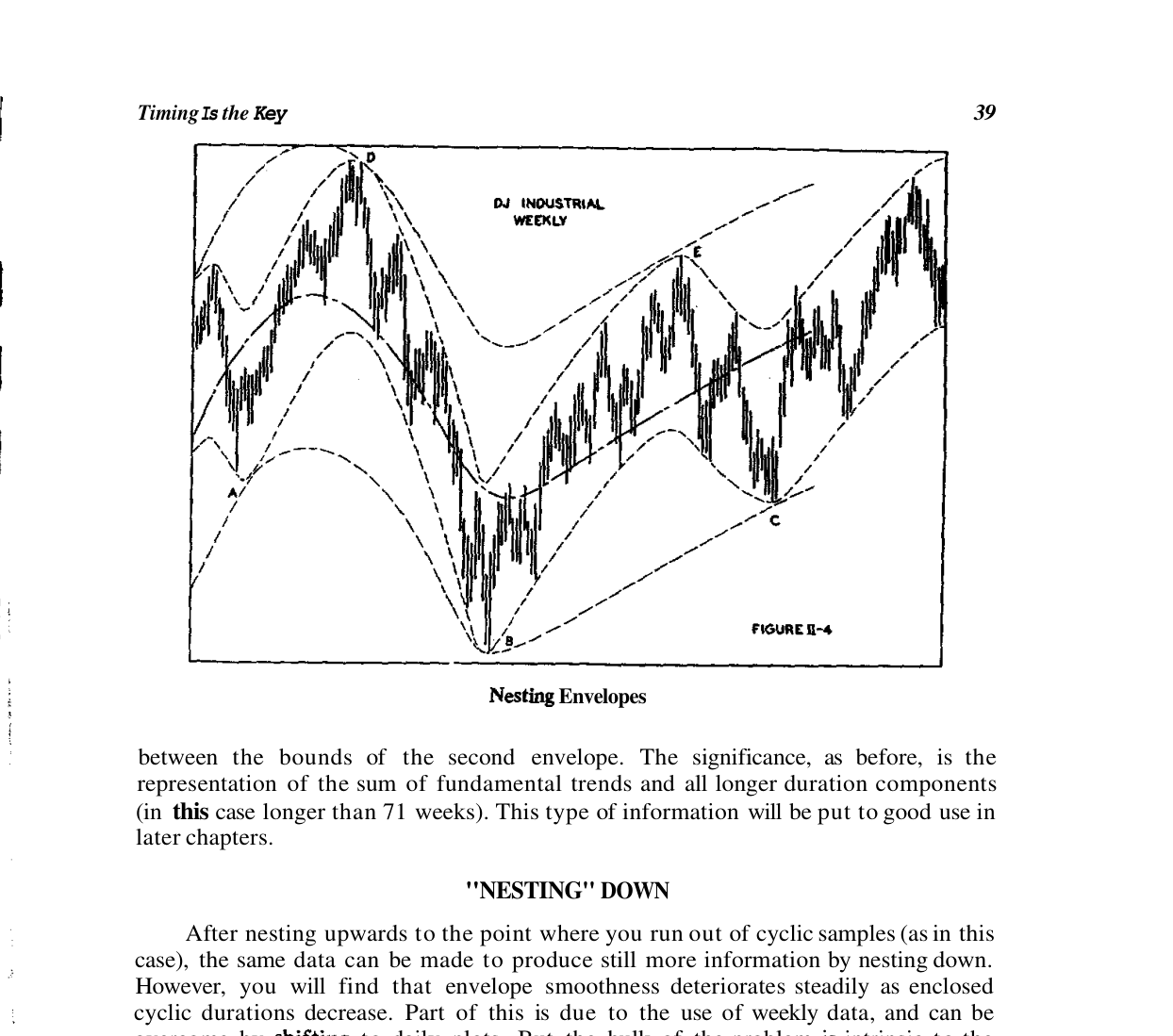

In plain words — The first envelope oscillates too: up and down inside a larger band. Draw a second envelope around the first, same rules, and read the higher cycle.

The second envelope has exactly the characteristics of the first — constant width, encloses everything — but applies to the first envelope instead of the data. The first band swings between the bounds of the second, making contact at its extremes: counting the weeks between them measures the higher cycle.

In the book's sample (DJIA 1965–69) only two samples are available: 67 and 75 weeks, average 71 ± 4 — the current manifestation of the 18-month nominal (78 weeks). And the 9- and 12-month cycles the model expects in between? Present but "observationally insignificant" in that period on that index: the dominance clause of the variation principle, not a hole in the model.

As with the first envelope, the centre line between the outer bounds represents the sum of the trends and of all components longer than 71 weeks.

Nesting down — the sub-cycle

In plain words — Inside each span of the measured cycle, price does not climb smoothly: it "gallops". Count the gallops — usually three — and you have the sub-cycle. Then refine it with the segment envelope.

Going down the ladder, envelope smoothness deteriorates — partly from weekly data, mostly from variation itself. Hurst uses two techniques:

- Counting the "gallops" — between one low and the next of the 21.4-week cycle, price makes three visible swings: 21.428 ÷ 3 = 7.14 weeks, the expression of the 6.5 nominal.

- The segment envelope (Figs. II-5/II-6) — connect the weekly lows to each other and the highs to each other with short straight lines, run a centre line through, number and count the lows: 15 samples, average 6.766 weeks (± 0.8) — within 5.3% of the first estimate, and more accurate.

Example — Standard Packaging, same era: envelope → 4 samples of 18.75 weeks; segment envelope inside → 14 samples of 5.71. Ratio 18.75/5.71 = 3.28: once again about three sub-cycles per cycle. And the stock's 5.71 against the index's 6.766 is commonality plus variation, in a single number.

When to change scale

| Action | When |

|---|---|

| Expand (go daily) | The chart gives fewer than 6–7 data points per cycle of the target component |

| Contract (go monthly) | You run out of long-cycle samples — in the book, the log-scale monthly from 1949 reveals the 52 ± 1 month cycle (≈ 4.5 years) |

| Log scale | When the sum of trends and longer components is very steep |

Summary card

| Direction | How | Result in the book |

|---|---|---|

| Nesting up | Envelope around the envelope | 67 and 75 → 71 ± 4 wk (≈ 18 months) |

| Nesting down (gallops) | Count the swings per span | 21.4 ÷ 3 = 7.14 wk |

| Nesting down (segments) | Envelope of connected lows/highs | 6.766 ± 0.8 wk (15 samples) |

Links

- Curvilinear envelope — the first band and the centre line

- Hurst nominal cycles — where all these measurements land

- Five principles of the cyclic model — dominance and variation

- Hurst tradition — chapter index