Who this entry is for — All the spectral work was done on the Dow: does it hold for your stock? The appendix answers with a single "really incredible" chart — and with an argument that demolishes, in passing, the idea that earnings drive the oscillations.

Source: J. M. Hurst, The Profit Magic of Stock Transaction Timing, Prentice-Hall, 1970 — Appendix II, Extension of "Average" Results to Individual Issues (pp. 201–203, Fig. A II-1).

Prerequisites

Appendix I — the spectral signature generalized here.

Newton's method

Proving that the Dow's spectral signature holds for every issue seems overwhelming — but it is the problem of every generalization: "Newton's famous law concerning the force of attraction between masses could scarcely be verified for every mass in existence". The procedure is physics': observe on a small sample (the DJIA), extend to as large a sample as practicable (here), then force the model to produce verifiable predictions (the predictive results of the chapters).

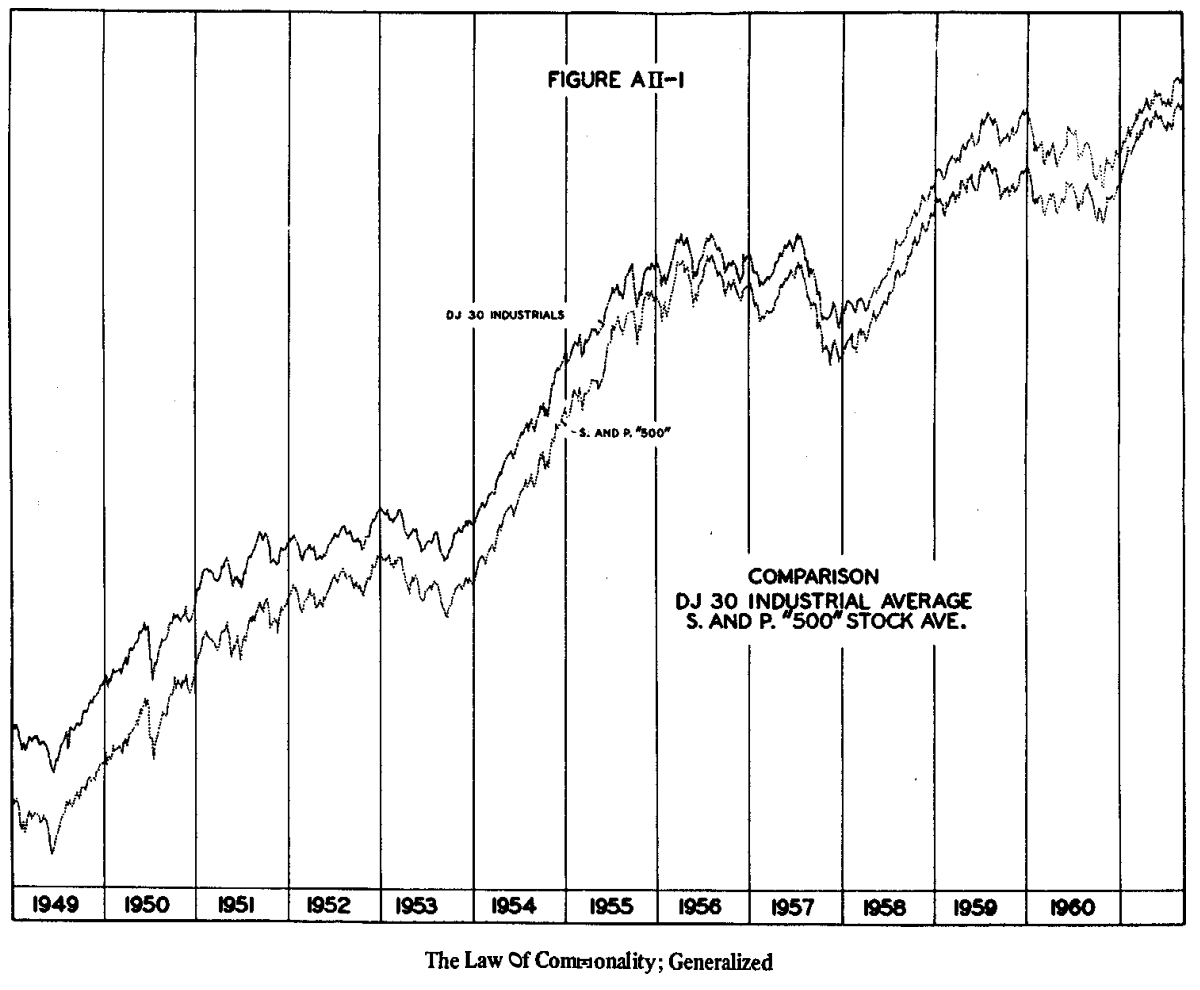

The incredible chart

In plain words — Dow and S&P 500 overlaid on a log scale, 1949–1961, one scale factor to equalize volatilities. Follow any fluctuation in one, and you find it identical in the other — down to the finest detail.

The implications, verbatim: the two averages' time series are so nearly identical that only minor spectral differences are possible between them; hence everything derived on the DJIA applies, with at most minor variations, to at least one-fourth of all issues on the NYSE and AMEX. And it is true "down to the finest detail resolved by weekly data" — and can be shown for daily data too.

The argument that demolishes fundamentals

At any given moment, the earnings and prospects of the S&P's 500 issues are in all possible states: some excellent, some terrible, every grade in between. If those considerations drove prices, an average of 500 issues should be smooth, individual variations averaged away. Instead the average shows the same ordered spectral signature as the Dow — and the same one, in near-perfect synchrony:

"Those fundamental considerations that are widely held to be so very effective in causing price change — and in fact are used as the basis for stock purchases and sales by individuals and institutions alike — simply are not the principal reason for the price motion that occurs!"

What is left to fundamentals is already familiar: volatility (the scale factor removed before the comparison) and the long-term smooth motion the fluctuations ride on. And the near-perfect synchronization of turns between the two averages dramatically extends what Ch. 2 showed on a single stock: if phases differed significantly between issues, the averages' fluctuations would be "smeared" — and the identity between Dow and S&P would be simply impossible.

Summary card

| Element | Statement |

|---|---|

| Data | DJIA vs S&P 500, weekly, 1949–1961, log scale, volatility equalized |

| Result | Identical fluctuations to the finest detail (daily too) |

| Extension | Spectral signature valid for ≥¼ of NYSE+AMEX issues |

| Fundamentals | Do not average the oscillations away → not their principal cause |

| Their residue | Volatility + long-term smooth trend |

| Synchrony | Near-perfect — otherwise the averages would be "smeared" |

Links

- Appendix I — the signature generalized here

- The five principles — commonality as a principle

- Historical events and cyclicity — the same argument on the macro front

- The appendices — index

- Hurst tradition — chapter index