Who this entry is for — Chapter 1 proves on one stock that shorter trades pay more. This appendix redoes the sum on 300 stocks and shows the curve that comes out — with the surprise of how steep it gets below ten weeks.

Source: J. M. Hurst, The Profit Magic of Stock Transaction Timing, Prentice-Hall, 1970 — Appendix III, The Source and Nature of Transaction Interval Effects (pp. 204–206).

Prerequisites

Hurst operating philosophy and Compounding and trading interval — the appendix is the empirical base of both.

Sample and method

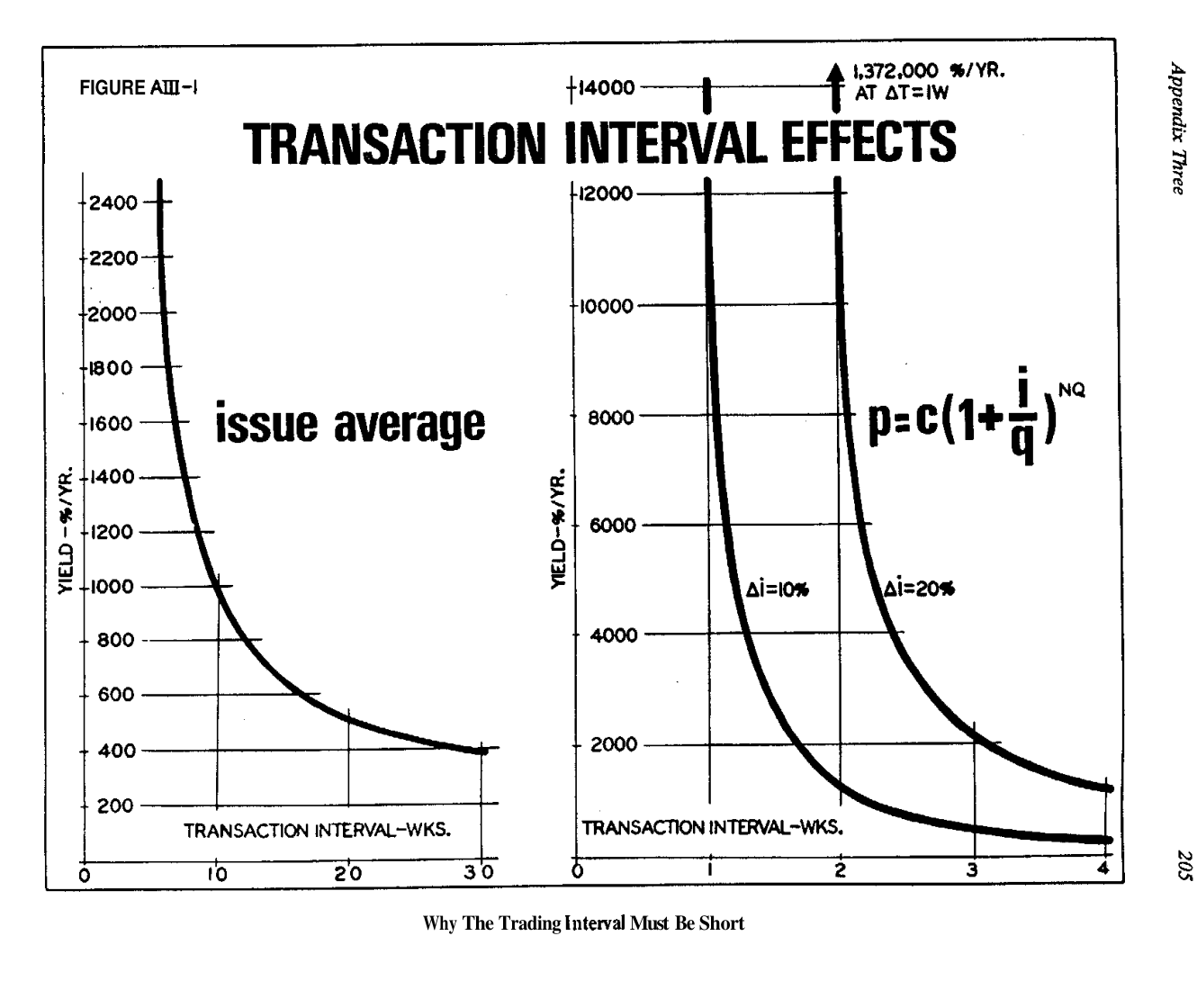

In plain words — Hurst takes 300 stocks at random, applies to each the same exercise done on Alloys Unlimited (perfect timing, ever shorter trades) and averages the results.

In Chapter 1 the interval effect had been demonstrated on a single issue. Here the procedure is repeated on 300 stocks selected at random, in equal numbers from the New York and American Exchanges. For each issue the theoretical maximum yield is measured as the average transaction interval varies (the weeks a complete trade takes); the results are then averaged: the resulting curve is the left panel of Figure A III-1.

Keep firmly in mind what the curve measures: theoretical maximums at perfect timing, with no commissions and no errors. It is not a promise of returns: it is a photograph of how much yield price fluctuations make available, as a function of how quickly you harvest them.

The "knee" between 10 and 20 weeks

In plain words — Above 20 weeks per trade, shortening changes little. Between 20 and 10 it starts changing a lot. Below 10, every week shaved off makes the potential yield soar.

The curve, Hurst writes, is inversely exponential, with a significant "knee" between 10 and 20 weeks: to the right of the knee it is nearly flat (around 400% theoretical per year at 30 weeks); to the left it climbs — already ~1,000% at 10 weeks, and below ten weeks the rise becomes very steep.

The operating conclusion is verbatim and unequivocal:

"It is worth almost any resource expenditure required to achieve significant shortening of average transaction intervals." (p. 204)

Where the shape comes from: compounding

In plain words — That curve is no market quirk: it is the signature of compound interest. The more rounds per year, the more often capital multiplies on itself.

In the right panel of the same figure Hurst sets beside the data two curves drawn directly from the compound interest law — p = c·(1 + i/q)^NQ — one for an average profit of 10% per trade, the other for 20%. The comparison makes it obvious, in his words, that the empirical curve "derives its principal shape from the compounding effect".

The two theoretical curves also give the measure of how high the scale goes: at a one-week interval with +20% per trade, the theoretical yield exceeds one million percent a year — a value so far off the chart that the original plate marks it with an arrow (1,372,000%/yr; the exact sum, (1.20)⁵² − 1, gives ≈1.31 million %). The appendix closes by tying what remains of the shape — the part compounding does not explain — to the summation of the sinusoidal components of the cyclic model, the bridge to Chapter 2.

Limits and the correct reading

Warning — The curve says that potential yield grows as the interval shrinks; it does not say that shrinking always pays. The maximums are computed at perfect timing with zero costs: in practice, below a certain duration commissions and timing errors bite harder than compounding adds. The book's own real test bench (Ch. 8) operates at ~9.7 days per trade after building the whole timing apparatus of Chapters 2–7 — not before.

Three things to take away:

- The direction — accuracy being equal, the short interval beats the long one, and the advantage accelerates below 10 weeks.

- The mechanism — compounding gives the curve its shape, not some mysterious property of stocks.

- The order of works — first you build the timing (Chapters 2–7), then you shorten the interval. Inverting the order means paying the costs of high frequency without collecting its potential.

Summary

| Element | Value |

|---|---|

| Sample | 300 stocks (NYSE + AMEX, random, in equal numbers) |

| Curve shape | Inversely exponential, knee at 10–20 weeks |

| At 30 weeks | ≈400%/yr theoretical |

| At 10 weeks | ≈1,000%/yr theoretical |

| Below 10 weeks | Very steep rise (at 1 week, +20%/trade → >1.3M%/yr) |

| Origin of the shape | Compound interest law + sinusoidal summation (Ch. 2) |

Links

- Compounding and trading interval — the mechanism, with Chapter 1's numbers

- Hurst operating philosophy — why the interval is a tenet

- The 1968 trading experiment — the real test bench (~9.7 days/trade)

- Hurst appendices · Hurst tradition