Who this entry is for — The entry point to Hurst's book: what a cyclic trader aims to achieve, and why "buy low, sell high" alone is not enough.

Source: J. M. Hurst, The Profit Magic of Stock Transaction Timing, Prentice-Hall, 1970 — Chapter 1, Maximize Your Profits (pp. 21–27).

Prerequisites

None — this is the first entry on the Hurst path. After reading it, continue with Compounding and trading interval and Four pillars of the system.

The starting point

In plain words — Prices go up and down. If you understand when they are relatively low or high, you can earn far more than by holding a stock for years without a plan.

The chapter opens with the only statement about stock prices on which — Hurst writes — any two students of the market will agree without reservation: stock prices fluctuate. It sounds trivial; yet on that triviality rests an operational fact: more money can be made faster from those fluctuations than in almost any other way known — provided you know when the fluctuations will occur.

The second bar-room maxim, "buy low and sell high", turns out just as hollow the moment you question it: how low is low — when is low? In the preponderance of those "whens", Hurst observes, you can read the label on the profit faucet: timing. That is transaction timing, and the whole book is the attempt to make it measurable.

Example — A stock swings between €18 and €22 every few months. "Buy low" without saying when means buying at €21 and waiting for years: timing is the missing part.

Trading, not passive investing

In plain words — The classic investor picks a solid company and stays in for years. Hurst's trader enters and exits on the cycle: the dividend is not the profit engine.

Hurst places investing and trading at the two ends of a single scale — the ability to anticipate reversals. With zero ability, long-term investing is the least-risk course: you collect the dividend and hope capital losses do not cancel it. With perfect ability — unattainable — trading risk would be zero and investing would no longer make sense. The book's declared goal sits near the second end: timing accuracy around 90%.

Hence the first tenet of the philosophy, verbatim:

"We are in the market to trade — leaving dividends to help offset margin interest." (p. 22)

Card — Investing vs Hurst trading

- The investor's key question: "Is this a good company?"

- The trader's key question: "Has the favourable cycle started or ended?"

- Typical error: holding a losing stock because "it pays dividends"

Return per unit of time

In plain words — What counts is not just how much you make, but how fast. Doubling in 20 years is little; doubling in six months is another world.

Hurst explains it with two imaginary friends. The first buys at 20 and sells at 40: money doubled — but twenty years passed between the two trades, and 5% a year the local bank would have paid too. The second buys at 20 and sells at 40 within a year: 100% per year — but then finds no stock he likes for the next nineteen years. Over the twenty-year average, he too sits at 5%. Opposite paths, same verdict.

The moral is the second tenet: success is measured as profit per unit of time over the entire span of activity, not as a multiple on a single trade. Maximizing it takes two things at once: the percent-per-year yield of each trade, and capital usage as close as possible to 100% of the time (see Compounding and trading interval).

Numerical example — $10,000 → $20,000 in 20 years = +5%/yr. The same doubling in 1 year = +100%/yr. Hurst wants capital working almost always, not sleeping between trades.

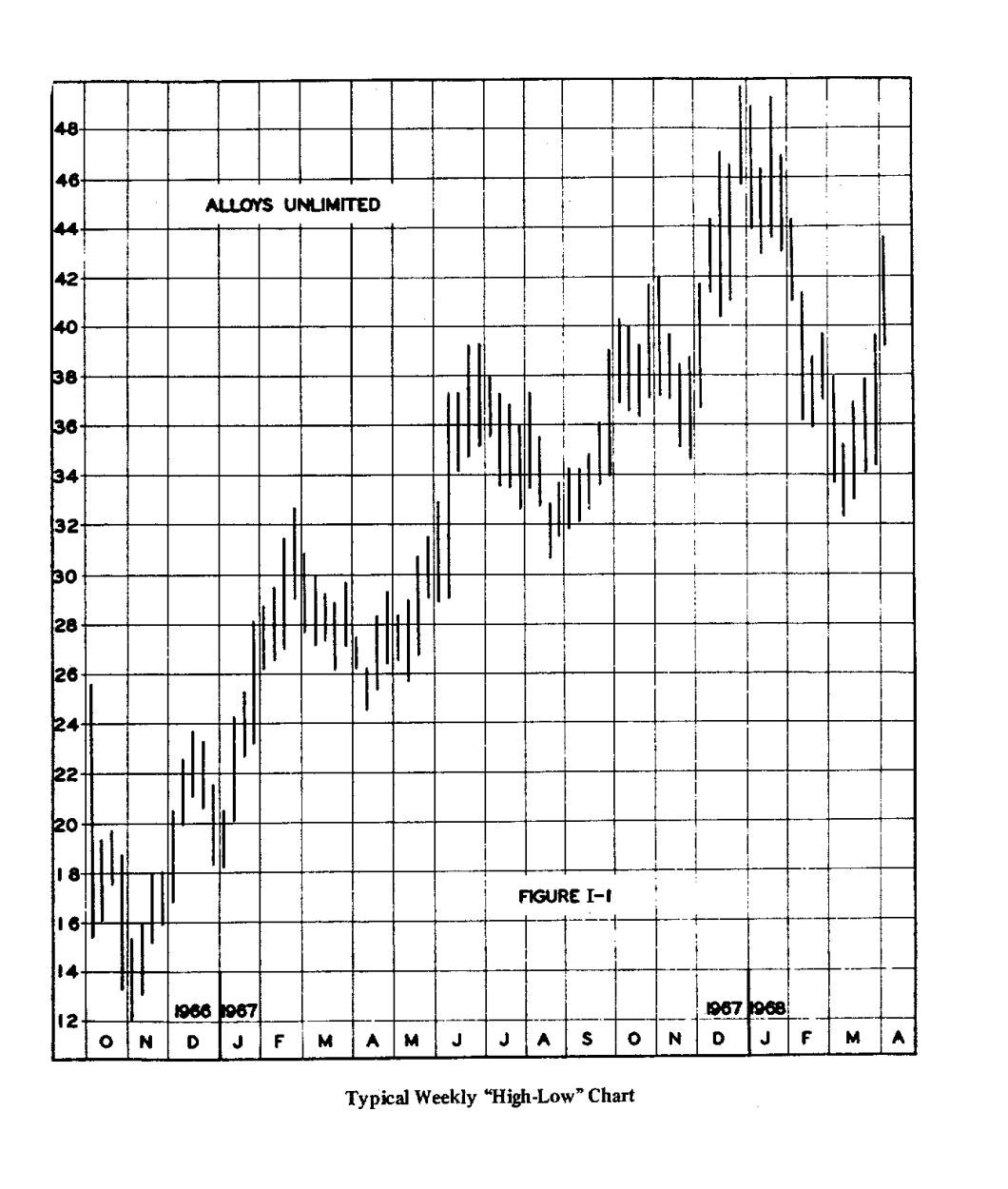

The demonstration: Alloys Unlimited

In plain words — The more complete rounds you close in the same period (buying at cycle lows, selling at cycle highs), the more capital multiplies on itself — and the return explodes.

The chapter's demonstration uses a real stock, Alloys Unlimited, over about 70 weeks (November 1966 – March 1968) and $10,000 of starting capital, under an assumption declared unrealistic — perfect timing — which serves only to make the three scenarios comparable:

| Scenario | Trades | Net profit | Equivalent yearly yield |

|---|---|---|---|

| One long round trip (plus final short) | 2 | $44,780 | 333% |

| The major reversals | 4 | $75,690 | 562% |

| All the reversals read (A–K) | 10 | $290,000 | 2,150% |

Same stock, same period, same rules: the only thing that changes is how many reversals you can read. Hurst attributes the effect to two causes: one is compounding (developed in Compounding and trading interval); the other is intrinsic to the nature of price motion — and understanding it takes the model of Chapter 2.

Objective signals

In plain words — Before entering the market you set clear rules ("if price does X, I buy"). When X happens, you act. No "in my opinion", no news of the day.

There is one last requirement, and Hurst motivates it with psychology before technique: timing rules must produce objective action signals, predetermined by analysis and triggered by actual price action — not by opinions, feelings or headlines. You decide beforehand; you execute when price says so. The theme becomes operational in Chapters 4–8.

Warning — An objective signal does not guarantee 100% success: the book's goal is ~90% timing accuracy. The remaining 10% is managed with stops and discipline (Ch. 4–5) — it is not eliminated.

Summary card

| Principle | In one line |

|---|---|

| Fluctuation | Prices rise and fall — the raw material of profit |

| Timing | When counts, not just how much |

| Trading vs investing | In and out on the cycle, not "buy and forget" |

| Return/time | Maximize yearly % and capital usage |

| Shorter trades | More complete cycles = more compounding |

| Objective signals | Rules written beforehand, triggered by price |

Links

- Compounding and trading interval — Ch. 1, the compounding engine

- Four pillars of the system — the map that closes the chapter

- Appendix III — Transaction interval — the 300-stock evidence

- Price motion model — Ch. 2, why prices swing this way

- transaction timing · action signal

- Hurst tradition — Hurst chapter index