Who this entry is for — Anyone who wants to understand why Market Profile «counts letters» instead of closes alone. Steidlmayer & Koy, *Markets and Market Logic* (1986), ch. 6.

Source: Steidlmayer & Koy, Markets and Market Logic (1986), Section I, ch. 6. Raw:

raw/patrimonio-emiciclo/studio-steidlmayer/mml/cap-06-osservazioni-comportamentali.

Prerequisites

Market Logic principles, Market-generated information.

Atomic unit

Product + participants + need + price + time → market activity. A TPO is a point in time when anyone can buy or sell at a specific price — the «atom» of market activity, as molecules are made of atoms.

| Element | Role |

|---|---|

| Price (vertical axis) | Promotes activity via excess |

| Time (horizontal axis, A, B, C…) | Regulates activity |

| Recurring TPOs | Acceptance → volume → value |

| Rare TPOs | Rejection → unfair price for one side |

Equation: price + time = market acceptance = transactional volume = value.

Timeframes and participant mix

| Type | Motivation | Market effect |

|---|---|---|

| Short timeframe | Must trade now | ~80% futures volume; seeks fair price today |

| Long timeframe | Exploits price away from value | Enter only at advantageous price; change condition |

Changing the timeframe mix is the only factor that changes market condition, increases volume, and moves price. Long buyers buy from short sellers when price moves far enough from value.

Stable trend: small, slow changes letting value follow price. Large, fast change attracts long timeframes that stop the trend (correction or range).

Volatility and dominant concern

Volatility depends on timeframe mix: when everyone trades short-term, the long «buffer» disappears → wide swings. The dominant concern is the worry absorbing short-timeframe participants; price neutralises it in the near term, often creating temporary excess. Dedicated entry → Dominant concern.

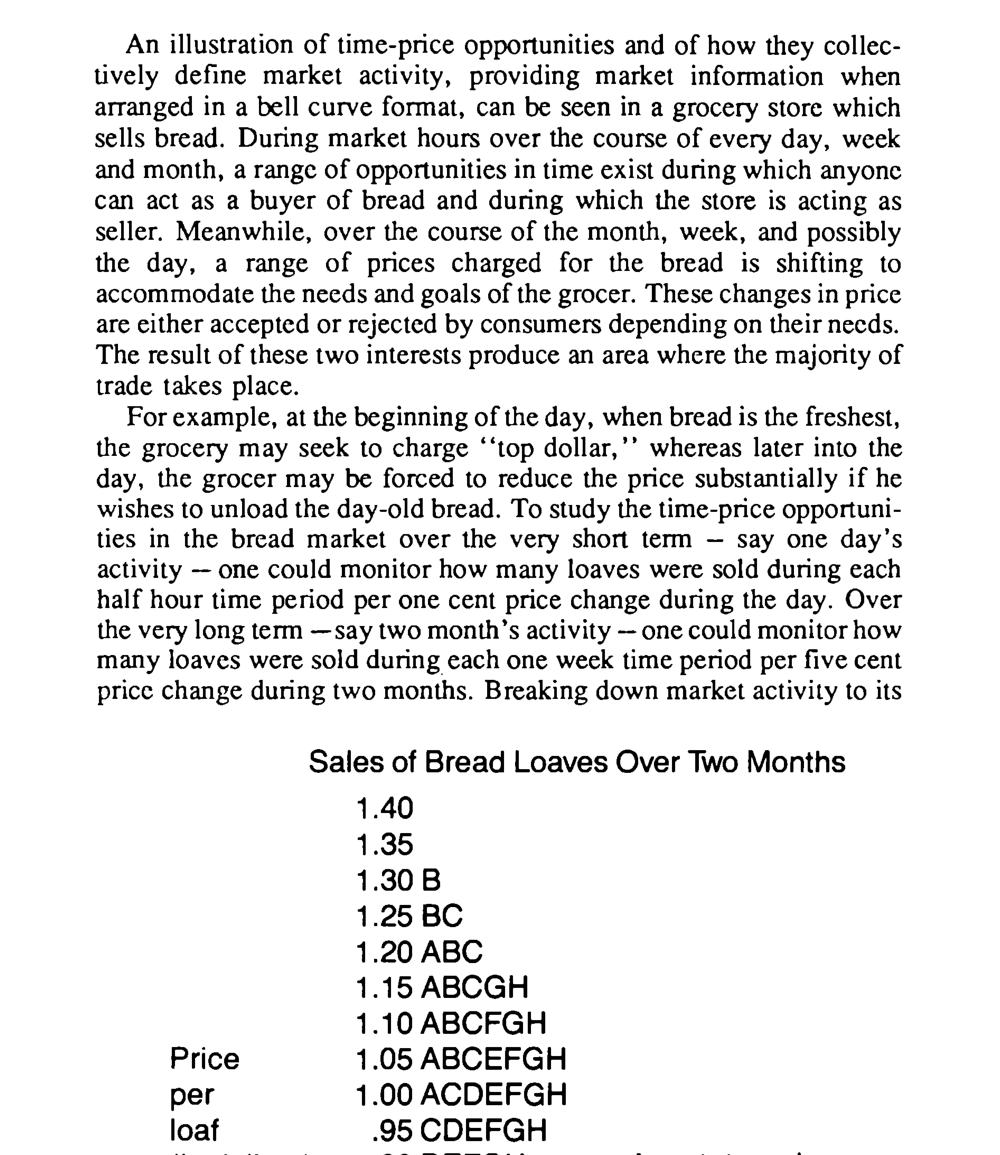

Bell curve — The studied period splits into time units (A, B, C…); each traded price accumulates letters. That is the graphic structure of Market Profile.

Acceptance vs rejection

- Long-recurring TPOs → acceptance/value for both sides.

- Brief TPOs → rejection; excesses above/below are offsets to find balance.

- Acceptance or rejection are known after the fact — benchmarks until change.

Guide example (auto executive): raising price, sales rise (acceptance); beyond a threshold they fall (rejection). The market says after the fact that price was too high — an «absolute temporary known», not a forecast.

Common mistake — Treating every price as equivalent. Willingness to accept one TPO over another is collective perception of fairness.